Без рубрики

6 4 The basic accounting for contributions

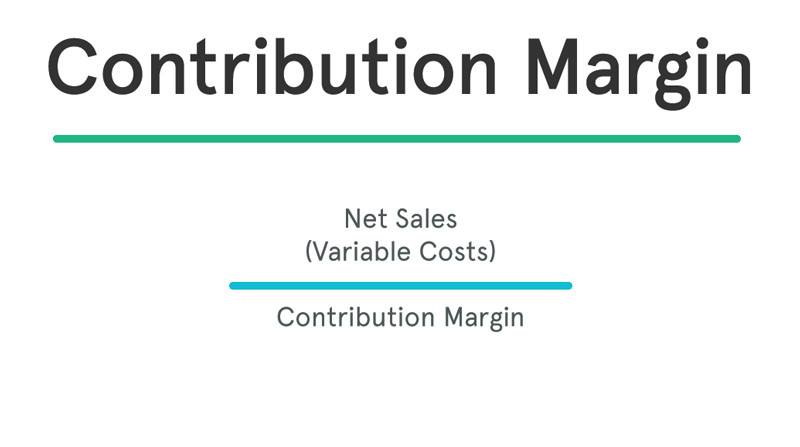

If a company has fixed costs (e.g. rent, insurance), the number of units must be large enough to cover these fixed costs before it can make any profit or loss. Once fixed costs are covered, then consideration should be given to whether there are still more units that could be sold. The contribution margin is computed as the selling price per unit, minus the variable cost per unit. Also known as dollar contribution per unit, the measure indicates how a particular product contributes to the overall profit of the company. In the most recent period, it sold $1,000,000 of drum sets that had related variable costs of $400,000. Iverson had $660,000 of fixed costs during the period, resulting in a loss of $60,000.

- At a contribution margin ratio of \(80\%\), approximately \(\$0.80\) of each sales dollar generated by the sale of a Blue Jay Model is available to cover fixed expenses and contribute to profit.

- If the company realizes a level of activity of more than 3,000 units, a profit will result; if less, a loss will be incurred.

- Variable costs are not typically reported on general purpose financial statements as a separate category.

- You will also learn how to plan for changes in selling price or costs, whether a single product, multiple products, or services are involved.

- Bravo Corporation (Bravo), a manufacturer of industrial products, pledged $750,000 for the event.

Gross Margin vs. Contribution Margin: An Overview

The gross profit margin is much more commonly used in the presentation of an income statement, and so is the figure most people see when they peruse an income statement. You would need to restructure such an income statement in order to determine the contribution margin. Iverson’s contribution margin is 60%, so if it wants to break even, it needs to either reduce its fixed expenses by $60,000 or increase its sales by $100,000 (calculated as $60,000 loss divided by 60% contribution margin). With a high contribution margin ratio, a firm makes greater profits when sales increase and more losses when sales decrease compared to a firm with a low ratio. Conceptually, the contribution margin ratio reveals essential information about a manager’s ability to control costs. The contribution margin may also be expressed as a percentage of sales.

Practice Questions

Instead, management uses this calculation to help improve internal procedures in the production process. The difference between the selling price and variable cost is a contribution, which may also be known as gross margin. Gross margin is synonymous with gross profit margin and includes only revenue and direct production costs. It does not include operating expenses such as sales, marketing costs, taxes, or loan interest. The metric uses direct labor and direct materials costs, not administrative costs for operating the corporate office.

Table of Contents

Fixed costs are often considered sunk costs that once spent cannot be recovered. These cost components should not be considered while making decisions about cost analysis or profitability measures. Another common example of a fixed cost is the rent paid for a business space. A store owner will pay a fixed monthly cost for the store space regardless of how many goods are sold.

Get in Touch With a Financial Advisor

The Contribution Margin Ratio is a measure of profitability that indicates how much each sales dollar contributes to covering fixed costs and producing profits. It is calculated by dividing the contribution margin per unit by the selling price per unit. Two ways a company assesses profits are gross margin and contribution margin.

Thus, at the 5,000 unit level, there is a profit of $20,000 (2,000 units above break-even point x $10). Managerial accountants also use the contribution margin ratio to calculate break-even points in the break-even analysis. Management should also use different variations of the CM formula to analyze departments and product lines on a trending basis like the following. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

Bravo Corporation (Bravo), a manufacturer of industrial products, pledged $750,000 for the event. The pledge document required ABC to perform specific activities, all of which are consistent with its normal operations. ABC agreed to identify Bravo as a sponsor contribution definition in accounting of the event on its website and in other communications and to permit Bravo to publicize its participation in its corporate advertising. Bravo did not receive any other benefits, such as free tickets to the event, as a result of this sponsorship.

In our example, the sales revenue from one shirt is \(\$15\) and the variable cost of one shirt is \(\$10\), so the individual contribution margin is \(\$5\). This \(\$5\) contribution margin is assumed to first cover fixed costs first and then realized as profit. Direct materials are often typical variable costs, because you normally use more direct materials when you produce more items.

Just as each product or service has its own contribution margin on a per unit basis, each has a unique contribution margin ratio. As you will learn in future chapters, in order for businesses to remain profitable, it is important for managers to understand how to measure and manage fixed and variable costs for decision-making. In this chapter, we begin examining the relationship among sales volume, fixed costs, variable costs, and profit in decision-making.

Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Likewise, a cafe owner needs things like coffee and pastries to sell to visitors. The more customers she serves, the more food and beverages she must buy. These costs would be included when calculating the contribution margin. Direct costs are any costs that vary directly with revenues, such as the cost of materials and commissions. For example, if a business has revenues of $1,000 and direct costs of $800, then it has a residual amount of $200 that can be contributed to the payment of fixed costs. Contribution margin looks similar to gross profit, which is sales minus cost of goods sold, but cost of goods sold includes fixed and variable costs.